Inflation has been a hot topic for millions of Brits over the past few years, as the cost of goods and services have risen sharply and put added pressure on many households.

According to Canada Life, inflation is a major worry for many Brits with their study finding that 83% of advisers cite inflation as the number one concern for their clients.

So, in the face of high inflation — and its eroding effect on the real value of your clients’ wealth — what options might they have to generate the growth needed to keep pace?

Two attractive options might be the Enterprise Investment Scheme (EIS) and Venture Capital Trusts (VCTs).

These investment vehicles for small start-up firms have the potential for greater returns for investors. However, they also come with their own set of increased risks.

Read on to learn about VCTs and the EIS, as well as two valuable benefits — and a few downsides — your clients should consider before opting to invest in either.

VCTs and the EIS provide opportunities to invest in start-up firms

VCTs and the EIS have provided investors unique opportunities to invest in exciting, fledgling firms for nearly 30 years (VCTs were launched in 1995 and the EIS was set up in 1994).

The EIS is a government backed programme designed to support the growth of small businesses

The government set up the EIS to encourage investment in small businesses, as this investment can lead to job creation and may stimulate economic growth in the UK. It offers a range of associated tax reliefs to incentivise investors to get involved with the scheme.

According to Octopus Investments, since the EIS was launched, more than 31,000 qualifying businesses have benefited from the scheme. They have received £22 billion of investment (as of HMRC figures from 29 May 2020).

VCTs are quoted private equity funds whose shares trade on the London Stock Exchange

Typically consisting of between 20 and 70 small, usually fledgling, companies — VCTs seek further investment to help these businesses achieve their growth and development goals.

These VCT-qualifying companies are not listed on the main London Stock Exchange and often have more potential for quick growth than their larger listed counterparts.

Clients invest in a VCT by buying shares in it and these shares then rise and fall in value, depending on the performance of the businesses within the trust.

All the above means that it is vital for your clients to consider the pros and cons of the EIS and VCTs before investing.

2 valuable benefits of investing in VCTs or the EIS for your clients to consider

1. There is the possibility of significant growth on your clients’ initial investment

The combination of firms within VCTs and the EIS being relatively small to start with, and being fuelled by investment funds that need to be spent on company growth, can lead to sizeable and potentially rapid growth in value for investors over the lifetime of the investment.

A few examples of successful companies to emerge from the EIS or VCT are:

- Everyman Cinemas

- Depop

- Five Guys

- Bought by Many

- Zoopla

These businesses have gone onto relative success and are now well-known, established brands. It is likely that savvy investors who moved their funds into these firms’ respective VCTs or EIS will have generated significant returns on their initial investment.

For example, according to Wealth Club, seven UK companies that have achieved “unicorn status” — when a company’s valuation exceeds £1 billion — received investment from a VCT or the EIS.

If your clients are looking for ways to gain significant growth on their investments — to help them tackle the effects of inflation on their wealth and reach their goals — it might be worth considering the EIS or a VCT.

2. The EIS and VCTs could offer significant tax benefits for your clients

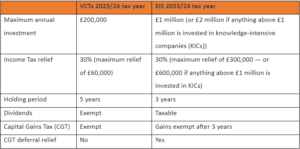

One of the main reasons why the EIS and VCTs are attractive to investors is the tax relief benefits provided on their investment, as shown by the table below:

If your clients are paying significant levels of Income Tax — and they’ve utilised the tax benefits of their pension Annual Allowance — they could consider pursuing further tax relief through investing in an EIS or VCT.

The respective relief on Income Tax, CGT, and Dividend Tax could be significant, especially for higher- and additional-rate taxpayers.

Read more: Could your clients save tax by investing in a Venture Capital Trust (VCT)?

Before investing in VCTs or the EIS your clients might want to consider the major downside

As mentioned above, companies within the EIS or a VCT are usually start-ups that are looking for additional funding to help them grow.

So, while they might have greater potential for rapid growth and success, they also conversely present a greater risk of failure, if the companies fail to achieve their goals and collapse.

Money Marketing reports that between 20% and 30% of investments in a typical VCT will likely not generate the expected returns. Money Marketing refers to investing in a VCT as “not for the fainthearted”.

Remember: VCTs and the EIS are higher risk, have a higher probability of losses, so it’s vital that your clients ensure that any investment aligns with their own tolerance for risk before opting to invest their hard-earned funds.

Get in touch

If your clients are interested in exploring new investment opportunities, a good first step could be to sit down with a financial planner to determine what options best suit their overall plans.

They should reach out to us by email at mail@delaunaywealth.com or call 0345 505 3500.

Please note

This article is no substitute for financial advice and should not be treated as such. To determine the best course of action for your individual circumstances, please contact us.

Enterprise Initiative Schemes (EIS) and Venture Capital Trusts (VCT) are higher-risk investments. They are typically suitable for UK-resident taxpayers who are able to tolerate increased levels of risk and are looking to invest for five years or more. Historical or current yields should not be considered a reliable indicator of future returns as they cannot be guaranteed.

Share values and income generated by the investments could go down as well as up, and you may get back less than you originally invested. These investments are highly illiquid, which means investors could find it difficult to, or be unable to, realise their shares at a value that’s close to the value of the underlying assets.

Tax levels and reliefs could change and the availability of tax reliefs will depend on individual circumstances.

Production

Production