The latest inflation figures from the Office for National Statistics (ONS) show that prices rose 9% in the year to April 2022 – the highest level of increase in four decades.

While you may be concerned about meeting the costs of rising prices, spare a thought for your children and grandchildren.

Research published by Moneyfacts shows that pocket money over the last couple of years has stagnated, with the average weekly pocket money received by a child in the UK standing at £6.14 in 2021, down from £6.18 in 2020.

Meanwhile, the prices of popular children’s goods like LEGO and PlayStation items have risen over the last year, according to the financial analysts.

While it’s unlikely that inflation will impact your children and grandchildren in quite the same way as you, it illustrates how rising prices can lead to challenges if your money is not keeping pace.

The unknown theft of inflation

In simple terms, inflation is when prices go up. This means that the items we buy every day – food, clothes, petrol – cost more over time.

In the UK, inflation is measured by the Consumer Prices Index (CPI). The CPI measures the cost of a basket of common goods and services, such as food and fuel. The Office for National Statistics (ONS) publishes the CPI every month and, according to the latest ONS data, the CPI rose 9% in the year to April 2022.

Inflation can be good for the economy as it encourages people to spend rather than save. However, when inflation is too high, it can be bad for savers as it reduces the value of their money in real terms.

Worryingly, many cash savers are unaware of the impact inflation will have on their money.

Indeed, recent research from Legal & General found that more than half of cash savers (52%) don’t know what rising prices mean for their cash savings.

Better start increasing your child’s pocket money allowance

When inflation is high, each pound you or your child has in their pocket will not be worth as much as it was in the past.

For example, if inflation is running at 9% as it is now, then a chocolate bar that cost £1.00 a year ago will cost £1.09 today. This doesn’t seem like much, but it soon adds up.

In the long term, inflation can have a very damaging effect on your child’s pocket money, as well as yours. If inflation remained at 9%, here is what the price of the chocolate bar would look like:

- Year 1: £1.00

- Year 2: £1.09

- Year 3: £1.19

- Year 4: £1.30

- Year 5: £1.41

As you can see, the price of the chocolate bar has risen by more than a third in just five years.

To combat the effects of inflation, you need to try and make sure that your own savings (and your child’s pocket money allowance!) keeps pace with inflation.

How to avoid inflation devaluing your money

As adults, there are a few things that you can do to help save your own pocket money from devaluing.

Move longer-term cash savings into equities

It is generally considered sensible to keep some cash – perhaps three to six months’ salary – in an easy access savings account by way of an emergency fund.

If you have more cash than you need, though, you could consider moving some into investments that could offer better long-term growth.

For example, equities typically provide a return that outstrips the interest you’d receive on cash savings.

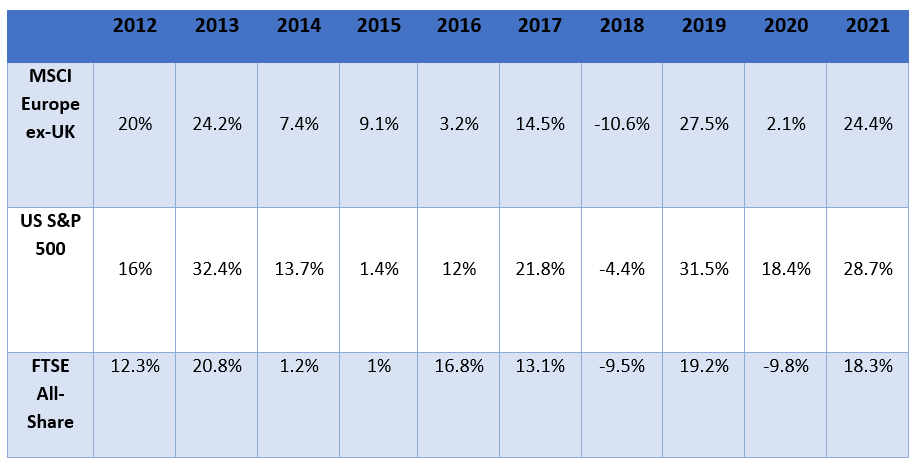

For example, the chart below shows the annual performance of major stock market indices in the UK, US, and Europe over the 10 years to 2021.

Source: JP Morgan. FTSE, MSCI, Standard & Poor’s. All indices are total return in local currency. Past performance is not a reliable indicator of current and future results. Data as of 30 April 2022.

You can see that, with the odd exception, markets produced positive, inflation-beating returns during this period, helping your wealth to retain its purchasing power over time.

We can help you to create a portfolio aligned with your long-term goals and attitude to risk.

Maximise tax efficiency

Another way of ensuring your savings are working as hard for you as possible is to make sure you’re saving and investing as tax-efficiently as you can.

ISAs allow you to put away as much as £20,000 in the 2022/23 tax year, and you won’t pay any Capital Gains Tax or Income Tax on returns.

In addition, saving into a pension could provide Income Tax relief of up to 45%, depending on your marginal tax rate.

Get in touch

We can help you put together a diversified portfolio tailored to meet your goals and circumstances. For advice on alternatives to cash saving, please contact us.

Email mail@delaunaywealth.com or call us on 0345 505 3500.

Please note

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Levels, bases of and reliefs from taxation may be subject to change and their value depends on the individual circumstances of the investor.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future results.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates and tax legislation may change in subsequent Finance Acts.

Production

Production