The Spanish-American novelist, George Santayana, once famously wrote: “Those who cannot remember the past are condemned to repeat it”.

The UK narrowly avoided entering a recession in Q4 of 2022, partly due to the winter World Cup and Christmas spending, with the Office for National Statistics (ONS) reporting no growth between October and the end of the year. However, the BBC reports that the UK is still projected to be the only major economy to enter a recession in 2023.

It’s concerning news for many Brits and is likely to cause your clients worries about their savings, investments, and mortgages. For those old enough to remember it, it might feel reminiscent of the 1990s and the economic downturn that affected many households.

But it’s important your clients remain calm. History can provide valuable lessons for facing familiar problems.

Read on to learn about the 1990s UK recession, how it affected people, and what your clients can do to protect themselves in 2023.

The 1990s saw an economic downturn and a period of “negative equity”

The UK’s rising inflation in the late 1980s prompted the Bank of England (BoE) to raise the base rate until it reached nearly 15% by the autumn of 1989. It would remain above 8% until the autumn of 1992 — double the base rate today, as shown by the table below:

Source: BoE

By the early 1990s the UK housing market had entered freefall as, according to Savills, property prices dropped nationwide by nearly 20% and mortgages became prohibitively expensive with interest payments hitting an unprecedented peak of 27% of buyers’ income.

This led to a “negative equity” situation for many homeowners, as the cost of the secured debt on their properties outweighed their current value.

While unemployment rose and markets saw short-term dips, the UK recession of the early 1990s was largely defined by the housing market.

3 useful ways your clients can gain property insights by learning from the 1990s

1. Mortgages swallowed up buyers’ monthly income — your clients might want to consider emergency funds and protection to help them should the worst occur

In the 1990s, the sharp rise in mortgage costs put a lot of households at risk, as payments ate up a huge portion of their monthly incomes. While the average house price was roughly four times the average annual earnings, today it is closer to nine times, as shown by the chart below:

Source: Schroders

The 1990s recession resulted in rising unemployment with the ONS reporting that the figure hit a high of 10.7% in late 1992. As households lost their income stream, mortgage payments were missed, and many were forced to default on agreements.

The Mirror reports that 345,000 homes were repossessed between 1990 and 1995.

Emergency funds and income protection are two possible options for your clients to consider. So, if the worst should occur and they are faced with outgoings they cannot meet, they have a financial safety net in place. It’s a move likely to provide significant emotional reassurance.

Setting aside an emergency savings fund — which would benefit from the currently rising associated interest rates on accounts — of ideally between three- and six-months’ worth of essential bills (such as rent or mortgage payments, utilities, and groceries) could cover any short-term needs your clients have if problems arise.

They could also consider taking out vital protection as an additional step. Income protection can help support your clients if there’s a sudden disruption to their income, such as an unexpected redundancy.

2. Mortgage rates rose considerably — your clients could consider reviewing their agreements and securing the best available rates

The inverse trend of rising mortgage rates and declining property values trapped many households in the 1990s in a state of negative equity.

Increasing mortgage rates made it difficult for many borrowers seeking to re-mortgage to secure a better deal. This situation was exacerbated by negative equity.

Many homeowners found themselves losing previously fixed rates on their mortgage as they matured and suddenly being exposed to much higher variable rates. Usually, a homeowner would seek a mortgage on more acceptable terms at this juncture.

However, negative equity meant the vast majority were unable to secure a new homeowners’ loan and were left vulnerable to high variable-rates until their properties were no longer in negative equity.

If your clients expect their current fixed-rate mortgages to mature in the near future, it might be worth securing new fixed-rate terms to avoid being exposed to high variable rates in the future.

Although many of the circumstances remain the same, the BoE reports some positive news as figures show the average UK household is much more financially resilient than those of the late 80s and early 90s.

3. Property prices dropped but eventually bounced back — your clients should be patient and not make any knee-jerk decisions

Downturns for investments can prompt fear-based reactions. It is a natural, human response and referred to as “loss aversion” — the concept that the pain of losses is felt twice as strongly as the joys of gains.

Property and mortgages are some of the most significant investments your clients are likely to make. In both cases, it’s important to take a long-term view.

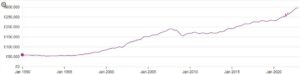

Markets typically rebound in the long term and the property market is no exception, as shown by the graph below showing the average property price in the UK:

Source: Land Registry Index

A study by Ocean Finance on Land Registry data between 2000 and 2020 showed a 78% increase in average property values for the period.

Your clients should consider their properties a “buy-and-hold” investment and look to retain them in the short term until prices bounce back in the future.

Get in touch

If your clients are worried about the looming recession and what the future might hold for their mortgages and property, they should seek out professional advice by emailing us at mail@delaunaywealth.com or calling 0345 505 3500.

Please note

This article is no substitute for financial advice and should not be treated as such. To determine the best course of action for your individual circumstances, please contact us.

Your home may be repossessed if you do not keep up repayments on a mortgage or other loans secured on it.

Buy-to-let (pure) and commercial mortgages are not regulated by the FCA.

Think carefully before securing other debts against your home.

Production

Production