The stock market isn’t the economy. Yet, many UK investors rely on it — and particularly the UK’s FTSE 100 and All-Share — as their only investing measure.

It can be a misguided perspective and may lead to your clients not accurately understanding the greater picture for their finances and investments.

The FTSE 100 is a share index of the 100 companies listed on the London Stock Exchange with the highest market capitalisation and can be a useful tool for judging investment performance.

However, it only accounts for a limited view of the greater marketplace and doesn’t track other global markets. It also has a vantage point fixed firmly on the future, whereas economic performance is judged on the past through to the present.

Read on to discover four powerful reasons why your clients shouldn’t rely on the FTSE as their only investing measure.

1. The performance of the FTSE can be different to other global markets

According to the Guardian, the FTSE 100 hit record highs on 3 February 2023 and has since broken records further. If your clients are using the FTSE as their key investing metric, it can paint a rather rosy picture.

However, the FTSE 100 is just a single stock market index on the London Stock Exchange. It doesn’t account for the performance of the wider UK market or markets around the globe.

If your clients have a smartly developed investment portfolio, it is likely to be well-diversified, which may mean that they possess assets in markets around the world.

Focusing too much on the FTSE can reduce your clients’ view of global markets. If they aren’t invested beyond the FTSE, they might be severely limiting the diversification potential of their portfolio.

A look at the performance of major global stock markets over the course of 2022 details differing returns, as shown by the table below:

Source: JP Morgan

While the FTSE All-Share saw positive returns for the year, the vast majority of other major global markets saw a downturn.

Focusing on the bigger, global picture can protect investments from downturns and help mitigate potential losses through expanded diversification.

2. Stock market indices like the FTSE don’t track the greater economy

Stock market indices are disproportionately made up of larger corporations. They don’t typically track smaller businesses that can be major drivers in the greater economy.

Read more: Why the stock market is not the economy

Stock market prices reflect investor confidence in the future, while economic indicators view spending and employment factors in the recent past and present.

If your clients’ portfolios contain investments in smaller businesses or assets outside of major corporations, stock market indices aren’t a great way to review their current and potential performance.

Your clients may benefit from speaking to an adviser about these investments and keep themselves apprised of micro and macroeconomic factors that may influence their long-term outcomes.

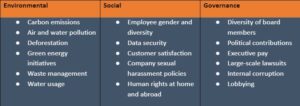

3. The FTSE doesn’t typically help as a barometer for specialist investments such as ESG funds

Your clients may want to develop investment portfolios aligned with their goals and closely held beliefs. This may involve investing in Environmental, Social, and Governance (ESG) funds.

ESG funds are comprised of businesses that have passed an assessment by an external agency that focuses on key criteria, as shown by the table below:

The larger stock market indices, like the FTSE 100, contain many industrial corporations in areas like oil and gas production, as well as firms in the defence industry. It is unlikely that many of these businesses align with your clients’ ESG goals.

So, an index that reports a strong outlook for fossil fuel companies might not offer the best insights into the future of eco-friendly firms.

4. Using the FTSE as a primary investing measure exposes your clients to additional risks

If your clients determine their investing preferences based purely on the performance of stock market indices like the FTSE, they could expose themselves to additional risks.

Stock market trends may project an increasingly optimistic or pessimistic view of investment potential. This could push your clients to be overconfident during periods when the markets are at a high, and potentially invest funds beyond their tolerance for risk.

Conversely, when the markets are in a downturn, your clients may feel negative about their portfolio’s future and decide to part with investments to reduce potential losses.

It is a short-term perspective, and investors typically benefit from a long-term view.

If your clients choose to lock in a short-term downturn in an asset’s market value by selling, they are converting what was a paper loss into a definite one, and they remove the possibility of the investment bouncing back in the long term.

Stock markets ebb and flow in the short term, but over longer periods of 5, 10, or 20 years they typically see positive returns.

In fact, the FTSE doesn’t even have to move to produce positive returns in the long term. Schroders found that even though the FTSE 100 closed marginally lower in December 2018 than the level it was at in December 1999, it could still have produced returns of almost 94% for investors provided they had reinvested their dividends.

Get in touch

Successful investing typically requires a grasp of the bigger picture and a long-term outlook. If your clients are preoccupied with short-term stock market trends, they may lose sight of their investments’ actual performance and how it factors into their plans.

Your clients might benefit from seeking advice, by emailing mail@delaunaywealth.com or calling us on 0345 505 3500.

Please note

This article is for information only. Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

Production

Production